Retail

One Shocking Report, a Few Bold Investors & Happy H1 Numbers

by

Robb Young | September 06, 2010

An analysis of the latest luxury news highlights

Counterfeit Catastrophe

Of all the places for a highly controversial luxury industry news story to break, an Oxford University academic journal would probably be the last place you look. But thanks to reporters at The Daily Telegraph who picked up on research published in The British Journal of Criminology, people were alerted to this hot bit of intellectual property news.

To the astonishment of many, a report funded by the European Union and co-authored by an adviser to the British government’s Home Office (the ministry in charge of security and the police) has concluded that counterfeit luxury goods are a benefit to the companies being copied and that the police should not waste their time fighting the illicit trade. Needless to say, this should ruffle a few feathers in the coming weeks. In fact, we’re rather surprised that it hasn’t already caused more of a furore given the respectability of the journal and researcher involved. For some initial reactions from a few leading luxury firms, peruse a follow-up piece in Brand Channel. Could such a report be seriously damaging by reopening a debate we thought was firmly shuttered? Or is this little more than a bump in the road leading to further progress in the anti-counterfeiting campaign?

Investors, Speculators & Stocks

Emperor Watch & Jewellery sells Vacheron Constantin, Baume & Mercier, Jaeger-LeCoultre, Cartier, Piaget (all Richemont brands) among others

The biggest headline of the week began with an analysis in the Financial Times and continues to revolve around the investment by LVMH’s investment fund, L Capital Asia, in Emperor Watch & Jewellery. Although the HK$240m (US$31m) injection will only represent a 6.9% stake in the Chinese retailer of fine jewellery and timepieces, it is interesting because many of the international brands currently sold across Emperor’s 30 outlets are owned by LVMH’s rival, Richemont. L Capital is a separate entity from LVMH and, as a private equity vehicle, it is expected to sell up, cash in and move on in about five years time. But one does wonder how much of the motivation behind the deal is strategic – in order for LVMH hard accessory brands to elbow in on Richemont’s existing distribution network. Emperor could add between 50-100 new stores around the country by the time L Capital departs.

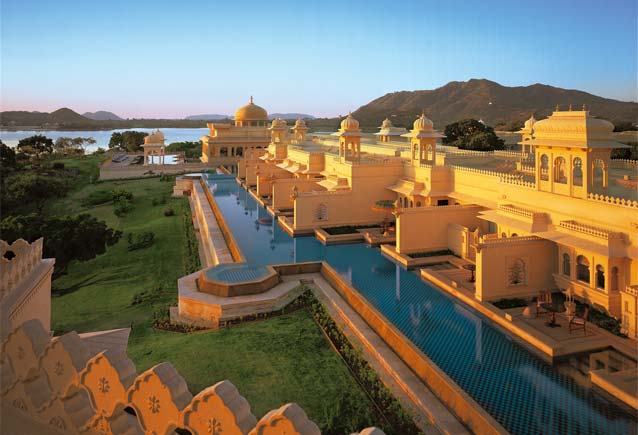

There has been a lot of talk about potential investments this week. The chairman of India’s largest diamond and jewellery manufacturer/retailer, Gitanjali Gems, told the Business Standard that the firm is close to acquiring a “leading Italian jewellery house,” which would be another trophy for the emerging market corporate fraternity (which now includes Tata and Zhejiang Geely) keen to own Western luxury brands. Incidentally, the Financial Times devoted an entire article to this last week. This followed one important confirmed deal in M&A; news – the 14.12% stake made by India’s Reliance Industries Ltd in the Oberoi hotel chain, as reported by Bloomberg.

The Oberoi Udaivilas Hotel in India

One rumour that just won’t go away is of LVMH’s alleged interest in buying a stake in the young American fashion brand Rodarte. WWD referred to “market sources” who say that the two parties are in a new round of negotiations, though neither side has confirmed that they are closer to a break-through. Any deal between the two would mean a major departure for Bernard Arnault, LVMH’s chairman, who has shied away from up-and-coming names and the apparel category in favour of accessories and heritage brands.

Similarly, Reuters has given further credence to speculation posited by the Daily Mail that a consortium of American and British private equity firms are poised to launch a bid for the listed department store chain Saks Fifth Avenue. Most analysts agree that Saks is an attractive target but its current top two shareholders, Mexican billionaire Carlos Slim and Tod’s owner Diego Della Valle, would make for a tricky transaction at the stock market.

Optimistic Earners

Miu Miu eyewear campaign, FW 2010/11 (one of Luxottica’s licensed brands)

If the scattering of recent H1/Q2 earning announcements provide an accurate reading of the wider industry, then the overall health of luxury is indeed looking much better than it was a year ago. Besides perennially rosy firms like Hermès, for which Market Watch estimated a 55% H1 income rise on 23% higher sales, there are a number of other bellwether brands raking in the profits.

Most encouragingly perhaps are those focused on entry level items at the other end of the spectrum like L’Oréal. Bloomberg credited part of the company’s 21% profit increase with the recovery of its luxury fragrance and cosmetic divisions: “Operating profit as a share of sales at the luxury division, which includes Armani cosmetics and Lancome lipstick, widened to 18 percent, from 12 percent a year earlier.” At Luxottica, the market leader in licensed designer eyewear, The Moodie Report proclaimed, “For the first time in the history of the group, net sales for the quarter approached €1.6 billion, with net income reaching €150 million.”

Other firms enjoying rising figures include Tod’s where H1 profits are up 21.6% (WWD) and Tiffany & Co for whom net sales rose 9% in Q2 (Yahoo Finance) .

Redefining Luxury from the Outside In

Prestige HD Supreme Rose Edition TV by Stuart Hughes

We in the luxury industry are notorious for trying to pinpoint exactly how our customers redefine ‘luxury’ at every single juncture in their lives. Since the downturn, we’ve become particularly obsessed with realigning our raison d’etre over and over again to match the market research. But what this insular approach almost never seems to take into account is how the rest of the world feels about luxury. Surely, one definition must feed into the other.

Recently, two reports were published outlining how the definition of luxury is changing among the masses, which could have consequences in what luxury consumers expect. A New York Times piece citing surveys by Pew Research provided several interesting revelations, including the fact that “fewer Americans [now] consider a TV set a necessity [than before], but the portion of Americans who [now] think flat-screen TVs are a necessity is on the rise.” What it seems to suggest is that the psychological gulf is indeed widening between the highest echelons of society and the average consumer.

Meanwhile, a British lifestyle report by Mintel which was featured in The Guardian (“Little luxuries resist the downturn”) confirmed similar studies in recent months: “holidays are now seen as a ‘luxury’ item of spending by almost half of adults, which compares to just 38% having this view before the recession in 2007”. But with so many ordinary folks ready to call any holiday a luxury, this begs the question, how then does the luxury travel industry now raise the bar for the most discerning consumers and offer a true ‘luxury holiday’? In other words, shouldn’t we be paying a little more attention to the bigger context in order to better serve our niche?