Consumers

Chinese Luxury Consumers Abroad - A Missed Opportunity?

by

Ekaterina Lapshina | October 05, 2022

As Chinese individuals continue to relocate overseas, motivated more by recent lockdowns at home, should brands think more about how to connect with their Chinese luxury consumer abroad?

Since the pandemic began, the Mainland China market has experienced a boom in business as it became one of the remaining active consumer markets in 2020. Now, two years later, China has experienced the second bout of COVID-19 cases since the start of the pandemic, drastically changing the consumer dynamics in the market. Nevertheless, Chinese luxury consumers remain an important audience for brands. Thinking about it differently, how might brands reach this group still? Over the last 5 years, the number of Chinese individuals relocating overseas has grown due to economic and “living environment” reasons, and more recently motivated by the lockdowns seen in the mainland market. For luxury brands looking to understand and learn more about their different Chinese consumers, the starting place may be closer to home. DLG decided to explore the untapped potential of luxury Chinese consumers living abroad, and ask - are brands overlooking an opportunity right in front of them?

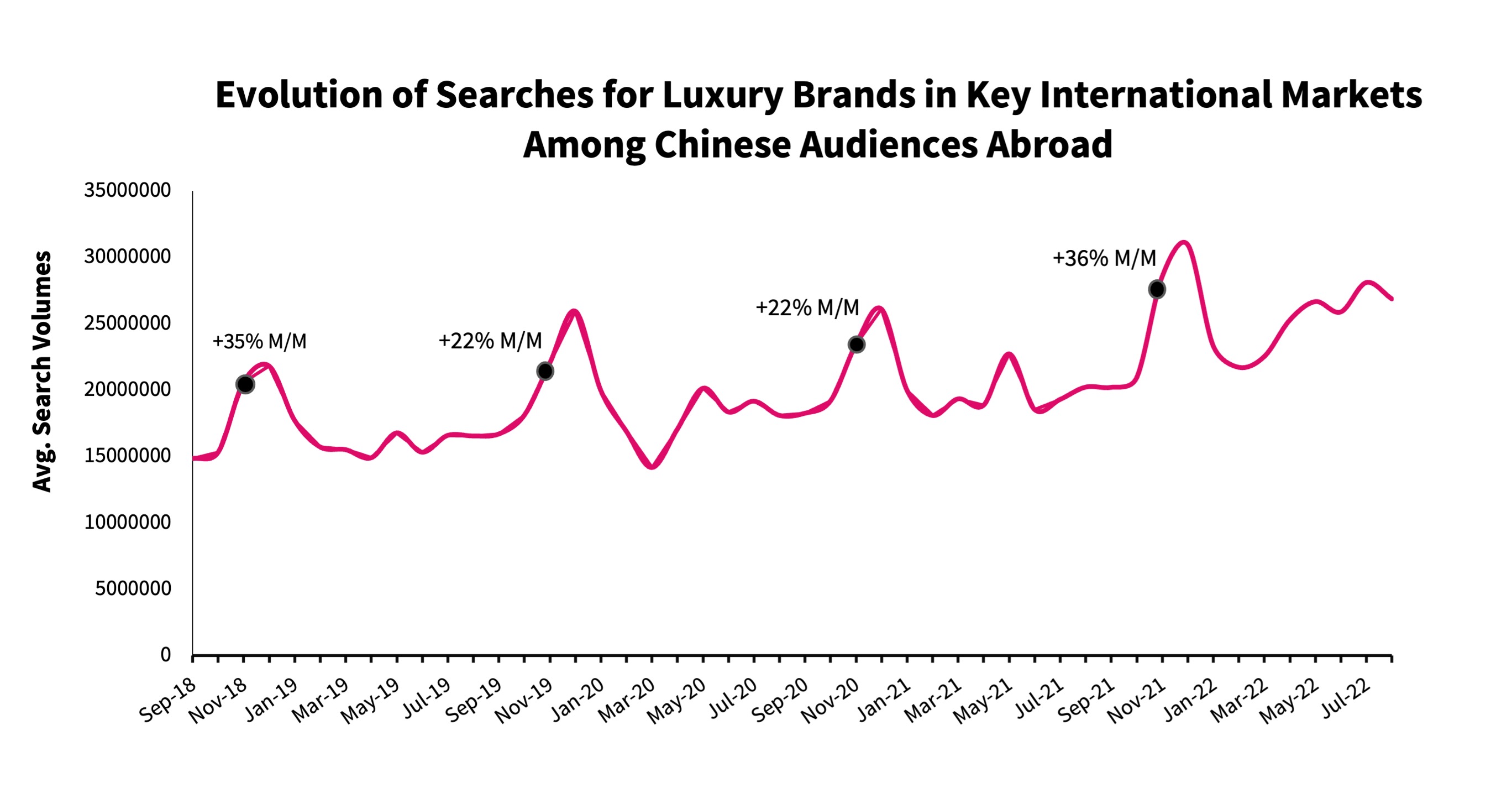

DLG conducted an ad-hoc research exercise to look at the search trends among users (with browsers set in the Chinese language) across key international markets for luxury brands. The sample of brands spanned 3 luxury categories including fashion, beauty, and watches & jewellery, including emerging and established brands within each. The research looks at search patterns on Google over three whole years, comparing pre-pandemic (2019) and post-pandemic (2021), as well as looking at current audience pool sizes on Meta platforms (Instagram and Facebook) to understand the potential target audience reach.

Overall search demand for the three categories continues to grow on average by 23% in major markets like the United Kingdom, United States, and France. Turning to audience size, the major markets remain as epicentres for luxury Chinese consumers. However, brands should also consider macro migration trends to markets like the UAE – while currently contributing a smaller audience pool, they have seen an inflow of Chinese expatriates over the past several years and expect continued growth in these communities.

Fashion

Among the three categories, search demand in-language is highest for fashion with 21% overall growth since before the pandemic. Yet, drops were seen for a few brands. For one established Italian luxury brand, a 33% drop in search demand was seen in the UK and 28% in Monaco; as well as an 18% decline was noted in Italy, Switzerland and Australia. A similar decreasing trend was seen for an American luxury brand in Italy and the UK (decline of 18% since 2019, respectively). While major cities make up the largest audience pool, it is worth looking at surrounding tier two and three cities to increase the brand’s potential reach; in the United Kingdom, while London accounts for 35% with the largest audience pool for the category, Manchester and Birmingham would collectively add another 18%.

Watches & Jewellery

Although seeing the lowest overall search demand of the three categories, watches and jewellery has seen a significant increase of 31% during this period. This may reflect the interest in the resale market of this category and the volatility seen since COVID-19 began. Interestingly, the category has the largest audience on Meta versus other categories, and in major markets the female audience is 62% larger than male. Among which, the 25 to 40-year-olds cohort makes up the largest proportion at 53% (for the male audience, 51%). As this age group represents the main composite of potential target audience for watches and jewellery, brands should think about targeting their respective audiences earlier in the funnel where they begin their research through online sources.

Beauty

For beauty, search overseas in Chinese language grew by 22%, and 25 to 40 year old females constituting the largest audience size. However, similar to the fashion category, some beauty brands have experienced decreases in search demand in key markets. The research found notable decreases of nearly 20% in Italy for a luxury skincare brand and a fragrance brand, as well as a third brand in the skincare business seeing similar downtrends for their brand searches in the United States and Australia over this time period.

By looking at search analytics, brands can identify their Chinese consumer audience in key markets overseas, and create a more compelling consumer journey for them, whether on their website or campaign landing page or driving them to a store experience nearby. In this research piece, search volumes for luxury brands in November increased on average 29% month on month over the past three years, around the well-known local celebration of Singles’ Day on November 11 each year and popular activation period for luxury brands.

The Chinese luxury consumer’s digital experience abroad will range in behavior and level of activity as they straddle between two digital worlds. However, according to Benjamin Dubuc, Head of Search and Performance Marketing at DLG, “capturing the audience with the right assets will help brands to have a higher user engagement and conversion rate on the website.” Whether it is creating or leveraging existing (and relevant) in-language visual assets online, recognizing and celebrating relevant Chinese milestones, or establishing a direct communication line on a relevant platform, there are opportunities to acknowledge the luxury Chinese consumer abroad and strengthen the brand’s connection with them.

On Dealmoon, a social e-commerce platform serving expatriate Chinese communities, some brands have started to adapt their communications to the Chinese calendars, and audiences have responded positively, shares global vice president Rose Blackmore. “Brands are really starting to create additional and or bigger opportunities around traditional Chinese holidays like Qixi and Mid-Autumn Festival for instance, which has also accelerated spending,” she says. Despite inflation’s impact on consumer spend, Blackmore says they’ve seen their audience increase spending as well, evidenced with larger basket sizes and higher average item values.

If not already, brands interested in growing their presence among Chinese consumers should consider exploring the untapped potential in markets abroad. The lessons learned may help build capabilities and best practices to serve this audience, whether it is the Chinese consumers living abroad or the Chinese consumers that will return to travel retail in the future.