RED, the Chinese digital platform known for lifestyle sharing, has become a pivotal marketing avenue for luxury brands in recent years. This year, DLG (Digital Luxury Group), together with China's leading content technology company NEWRANK, launched the RED Luxury Index 2022 – the industry’s first benchmark for RED.

In recent years, China has seen the rise of various digital platforms. While RED has been on the radar of brands for some time, it was not until recently that it started to come under the spotlight. Given the demanding requirements from the luxury industry in terms of brand image and community environment online, the platform initially appealed largely to beauty brands. Today, however, hundreds of luxury and premium brands across the beauty, fashion and even watches and jewellery categories establishing a presence on RED, and actively interacting with this community.

RED began nearly a decade ago as a travel-focused social media platform. In recent years, the community has expanded from the travel industry to almost all consumer segments, with over 200 million monthly active users on this platform sharing their opinions on products and brands.

For luxury goods, the content on RED aligns with the brand's primary marketing goal – increasing desirability – and thus provides a marketing-friendly ecosystem for brands to tap into. In comparison to other social platforms, RED allows brands to not only drive awareness at the top of the funnel, but the UGC-driven environment also allows brands to leverage consumers to advocate for brands at the bottom of the funnel.

This year, DLG (Digital Luxury Group) has launched the RED Luxury Index 2022 in collaboration with NEWRANK, China's leading content technology company, and its RED data platform Xinhong. This report examines where brands stand across indicators like community, content, engagement, and commercial collaboration by analysing the performance of 157 luxury and premium brands across the Fashion, Beauty, Watches & Jewellery, and Wine & Spirits categories, with the goal of establishing key benchmarks for the luxury industry on this platform.

Overall Community

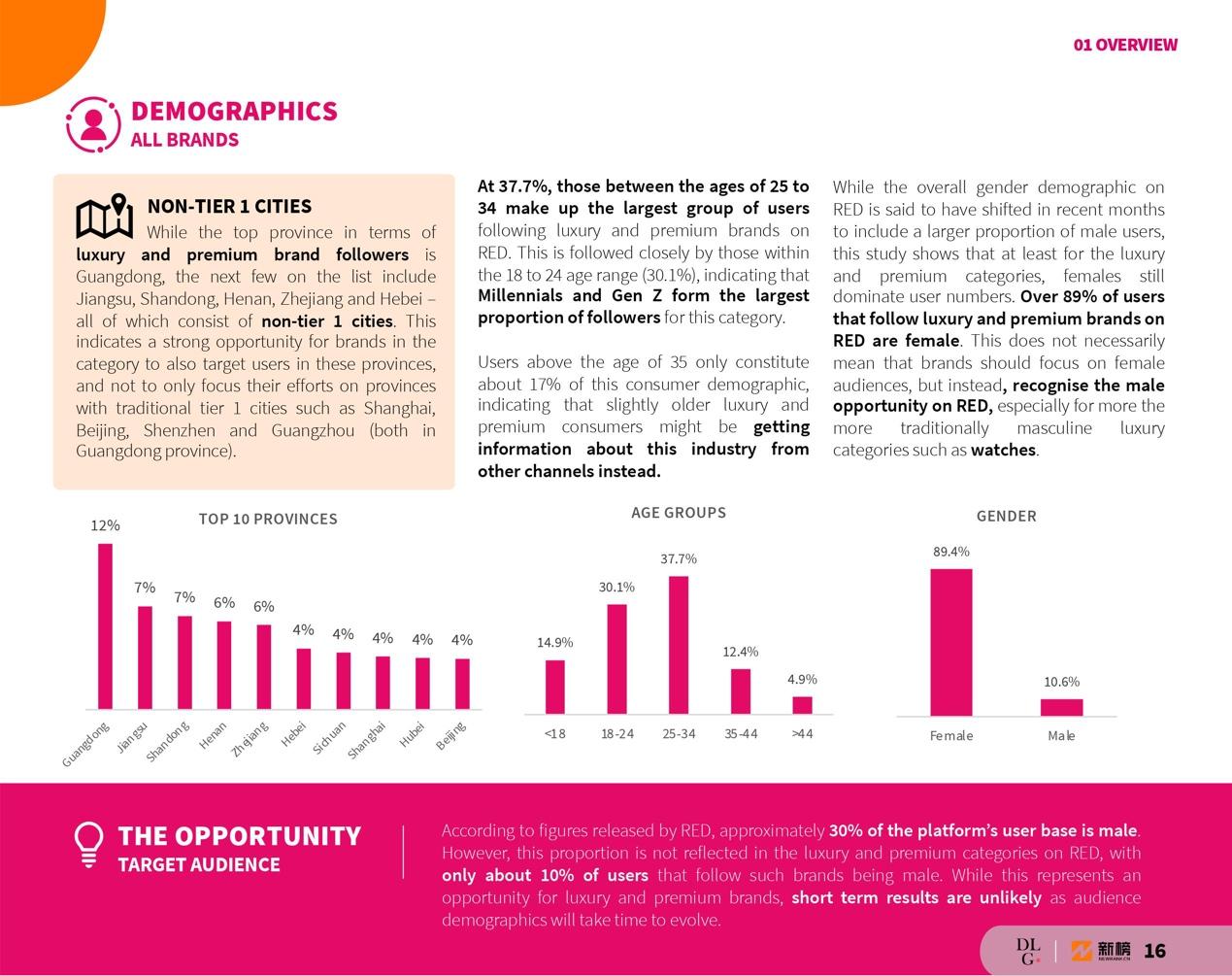

According to the data collected, the follower profile of luxury and premium brands is predominantly female (89.4 per cent), with ages ranging from 18 to 34 years old (67.8 per cent), and they generally are from provinces in first-tier and new first-tier cities.

It is important to note that in terms of geographical distribution, Beijing and Shanghai – traditionally the two most important first-tier cities – do not place among the top. Instead, the majority of followers come from provinces such as Jiangsu, Shandong, Sichuan, and Zhejiang, many of which are new first-tier cities. This suggests that luxury brands should not only target first-tier cities, but also new first-tier cities and even lower-tier cities to seek new growth.

The gender distribution here is also worth noting. According to official data released by RED, male users already account for 31 per cent of users on the platform. This, however, does not appear to be the case for the luxury and premium sector, as the sample data shows that male users account for only 10.4 per cent of the brands' followers. This suggests that there is still a significant opportunity for luxury and premium brands to reach out to the male audience on RED, particularly in more masculine categories such as watches and footwear.

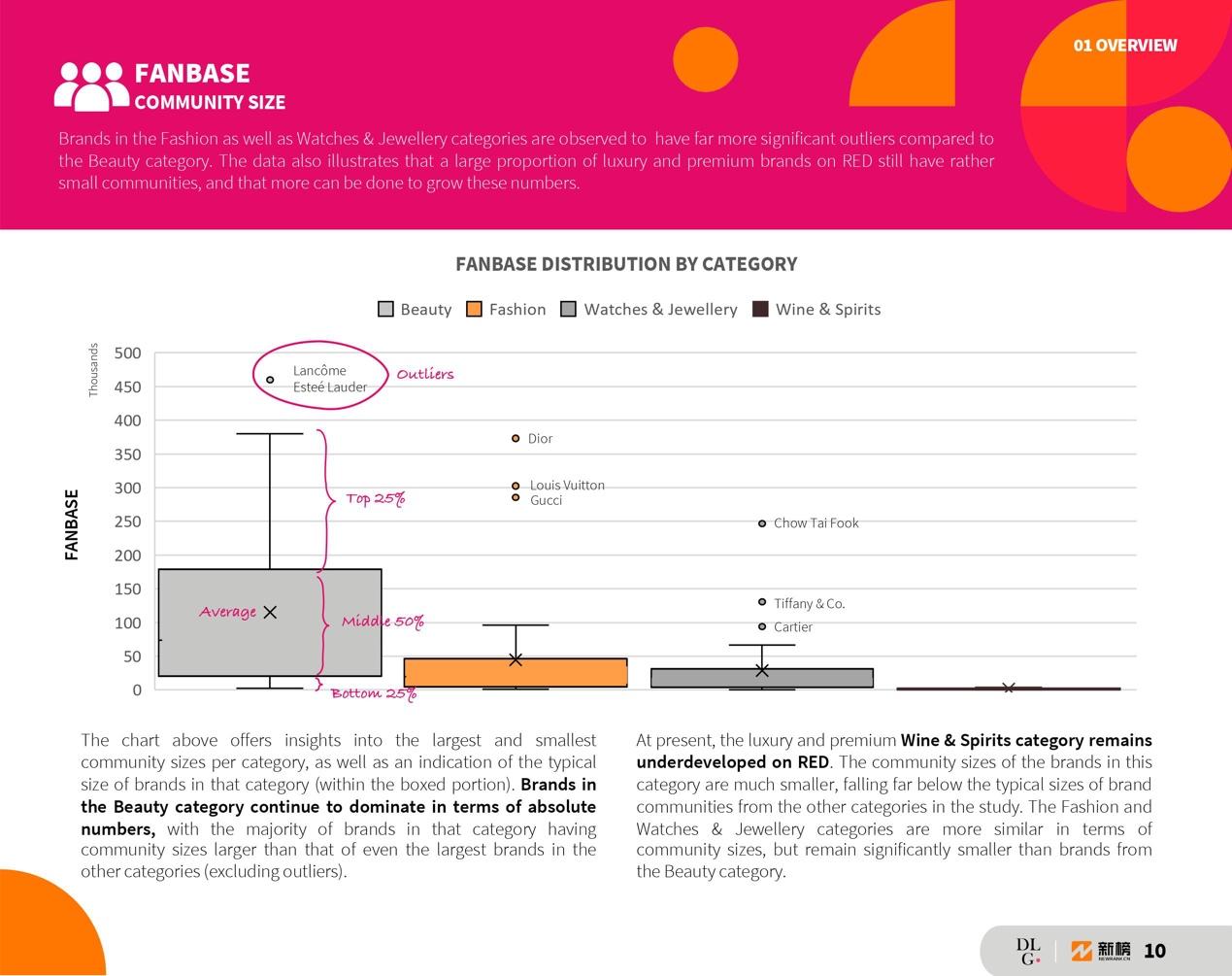

Seven of the top 10 brands with the largest fanbase are from the Beauty category, and beauty brands have much larger communities overall. However, the outliers in Fashion and Watches & Jewellery are on par with top beauty brands, demonstrating that these categories still have good growth prospects.

Market Dominance: Beauty Leads the Way, Fashion on the Rise

The large community sizes of beauty brands on RED are likely due to the category's early adoption of the platform, as well as its female-driven community. While this is one indicator of the category’s dominance on the platform, the report sheds light on others as well.

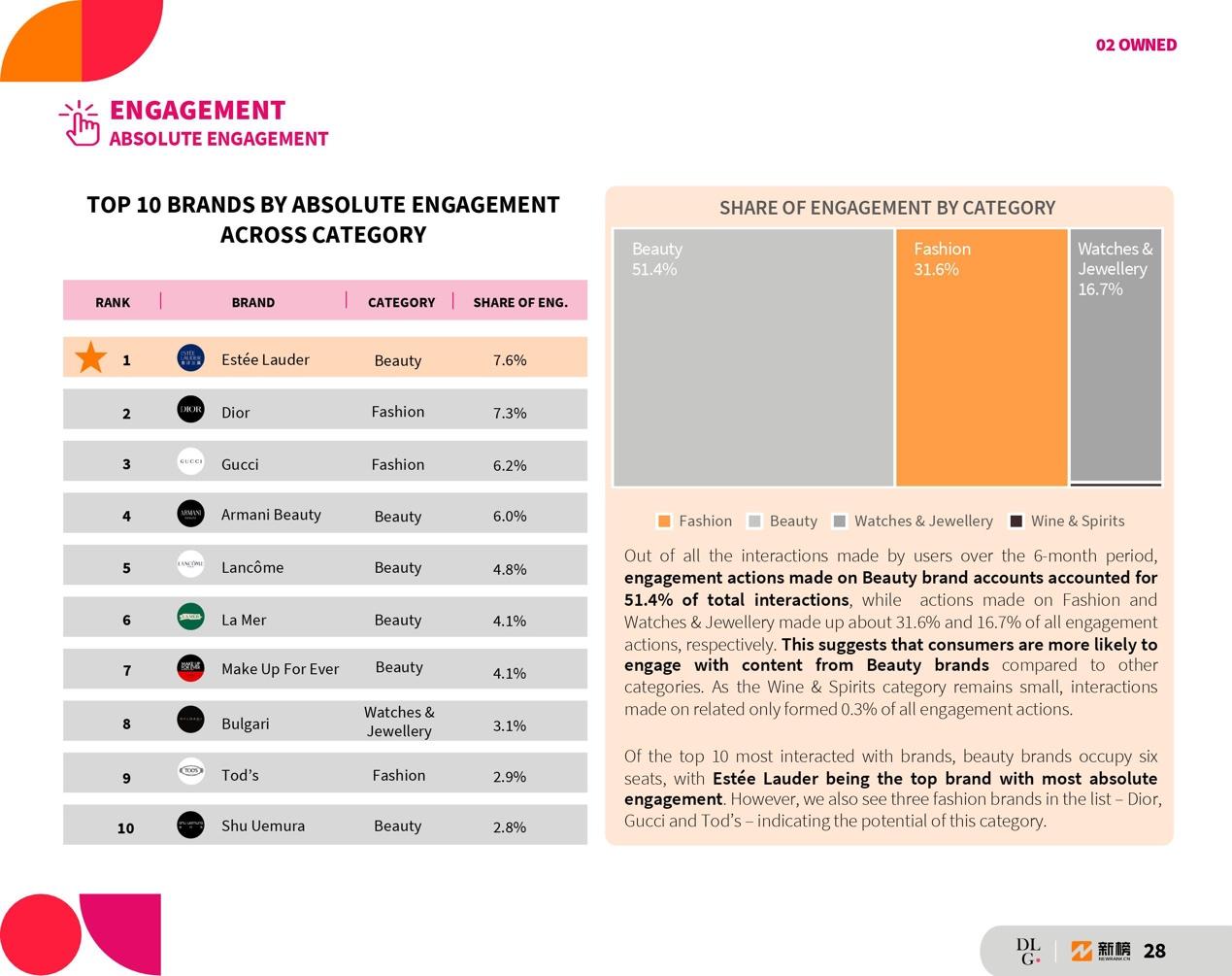

The report examined 157 brands' word-of-mouth posts (that include brand keywords) to determine each brand's share of voice on the platform. In terms of categories, beauty-related content accounted for over half of all the posts on the platform (50.25 per cent), while content about fashion and watches & jewellery accounts for 32.40 per cent and 16.97 per cent of the total, respectively.

It's worth mentioning that the share of voice distribution numbers is similar to that of another indicator: engagement. In addition to external channels, the report also examined the total engagement of brand-owned accounts and found that all beauty brands accounted for 51.4 per cent of total engagement actions across all the brands studied. While word-of-mouth posts and brand content performance are not directly correlated, they both reflect the level of penetration of each category among the RED audience.

When it comes to growth rate, however, Fashion has the fastest growing fanbase of the four categories, with Wine & Spirits and Watches & Jewellery following close behind. Beauty, which has the largest audience numbers, is becoming increasingly saturated as a category, with some brands even experiencing negative growth.

Marketing Cadence

Another key focus for brands on RED is the marketing calendar, which includes determining the frequency of brand posting and commercial partnerships.

In terms of posting frequency, all categories examined posted more frequently around key local marketing milestones such as New Year and Singles' Day. Each category posted more during specific category milestones – for example, a spike in content on fashion brand accounts was observed during the international fashion weeks.

However, a brand’s marketing calendar on RED does not necessarily have to mirror that on other platforms. According to Xinhong’s data, more than 40 per cent of content on RED continues to generate engagement after 30 days. This demonstrates that RED content has a longer lifespan than content on WeChat and Weibo, and that brands should take this delayed content traction into account when formulating communication calendars on RED, releasing content ahead of marketing milestones and allowing interest and desirability to build over time.

Collaborating with KOLs and KOCs

Qu Fang, Co-founder of RED, once stated that 97 per cent of the content on RED is user-generated content (User Generated Content). So in addition to focusing on brand-owned communities, brands should also leverage the platform's massive KOL and KOC pool to influence consumers' purchase decisions.

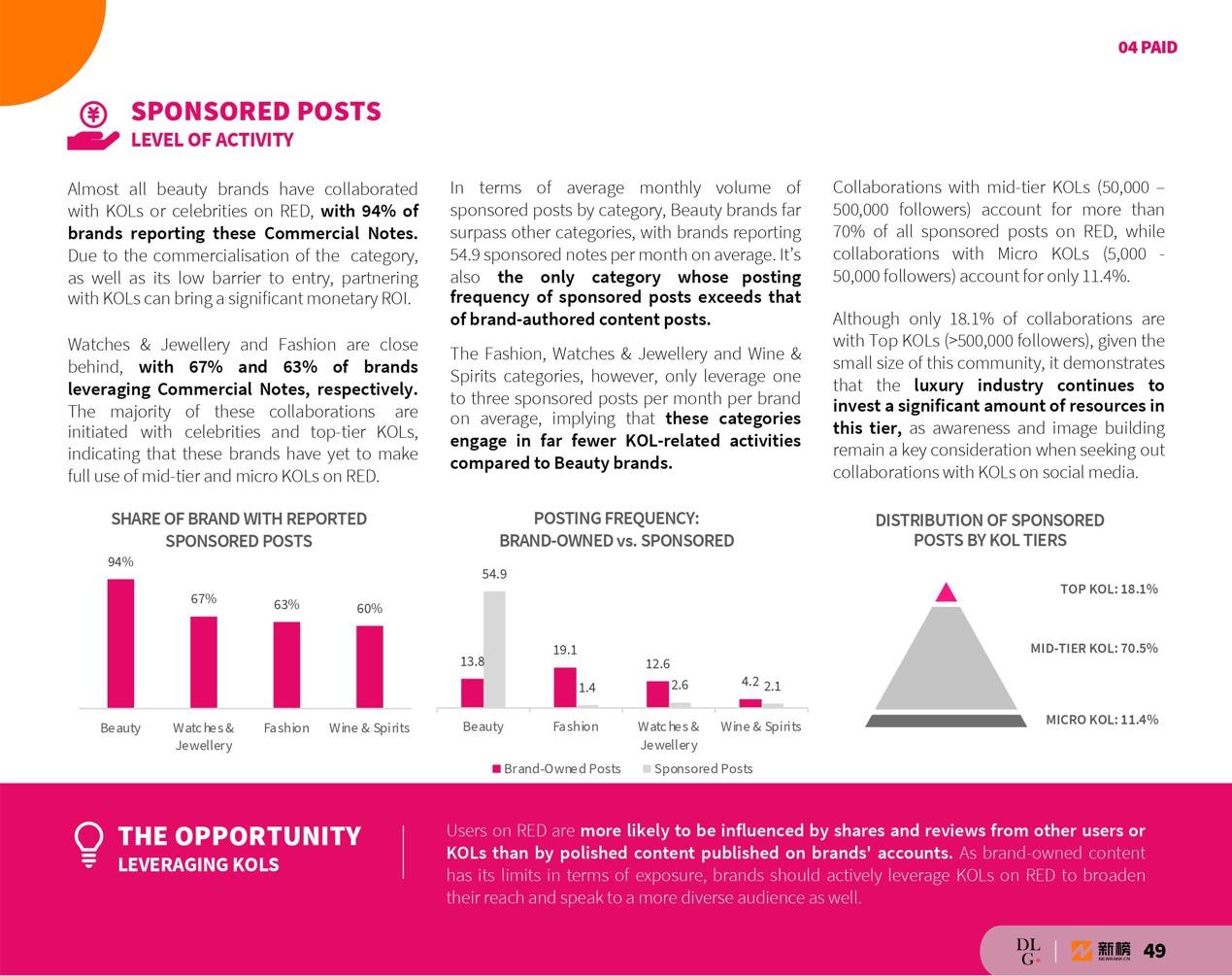

Based on the study, nearly 74 per cent of the brands have already carried out regulated partnerships with KOLs on RED via Pugongying (RED's official commercial collaboration platform). This indicates that the majority of luxury and premium brands are already leveraging external voices to increase awareness on the platform. It is worth noting that almost all (94 per cent) of the beauty brands studied have initiated sponsored partnerships on RED – a far higher percentage than any other category.

In terms of KOL tiers, Mid-Tier KOLs (50,000 - 500,000 followers) contribute the most sponsored content (70.5 per cent). Top KOLs (more than 500,000 followers), on the other hand, only contributed 18.1 per cent of sponsored content. The relatively lower volume of Top-Tier KOL collaborations (Xinhong data shows that the volume ratio between Top KOLs and Mid-Tier KOLs is 1 to 40) demonstrates that brands in the luxury segment are still willing to invest heavily in a small number of Top KOLs for greater image and quality content.

Paid KOL partnerships, however, are not the only way to raise brand awareness. According to the data collected, the majority of word-of-mouth content comes from KOCs. Brands can increase their share of voice on the platform by implementing tactics such as a UGC campaign, which encourages KOCs and regular users to share their lifestyles, at a reduced cost.

For full access to the brands ranked in the study and more insights on RED, watch a recap of the webinar launch and download the full RED Luxury Index 2022 at the link below.