Consumers

How Can Brands Seek New Growth as China’s Luxury Market Stagnates?

by

Alexander Wei | December 22, 2022

Luxury spending of Chinese consumers is expected to increase by 1 per cent in 2022, while the domestic market will remain stagnant. In the face of a potential shift in the local consumer landscape, how can brands identify market opportunities and maintain a consistent level of growth in the future?

The world is finally stepping out of the shadow of COVID-19 – at least for the majority of countries. In addition to the return of leisure travel, consumer markets have rebounded with the West's recovery from the pandemic and luxury companies reported notable results in the most recent fiscal quarter.

Thanks to the influx of tourists brought about by the weak Euro and Yen, major conglomerates such as LVMH, Kering, and Richemont all reported significant double-digit growth in Western Europe and Japan. Meanwhile, the North American market remains steady, and emerging markets such as the Middle East and Southeast Asia have picked up due to the resumption of leisure travel.

Amidst the global recovery, China has been unable to keep apace due to prolonged COVID restrictions and a sluggish domestic economy. According to the recently released Report on Digital Trends of China’s Luxury Market by BCG and Tencent Marketing Insight, the Chinese consumer luxury market is expected to grow by only 1 per cent to 530 billion yuan in 2022, well below the 23 to 25 per cent growth seen in 2021.

With the continued relaxation of China's COVID policies, a reopening appears to be on the horizon and brands must prepare for this change that will inevitably result in an additional loss of local luxury shoppers. However, given the current scenario, there are still audience segments and channels that make an impact on the Chinese luxury market. How can brands spot emerging opportunities?

A K-shaped Trend

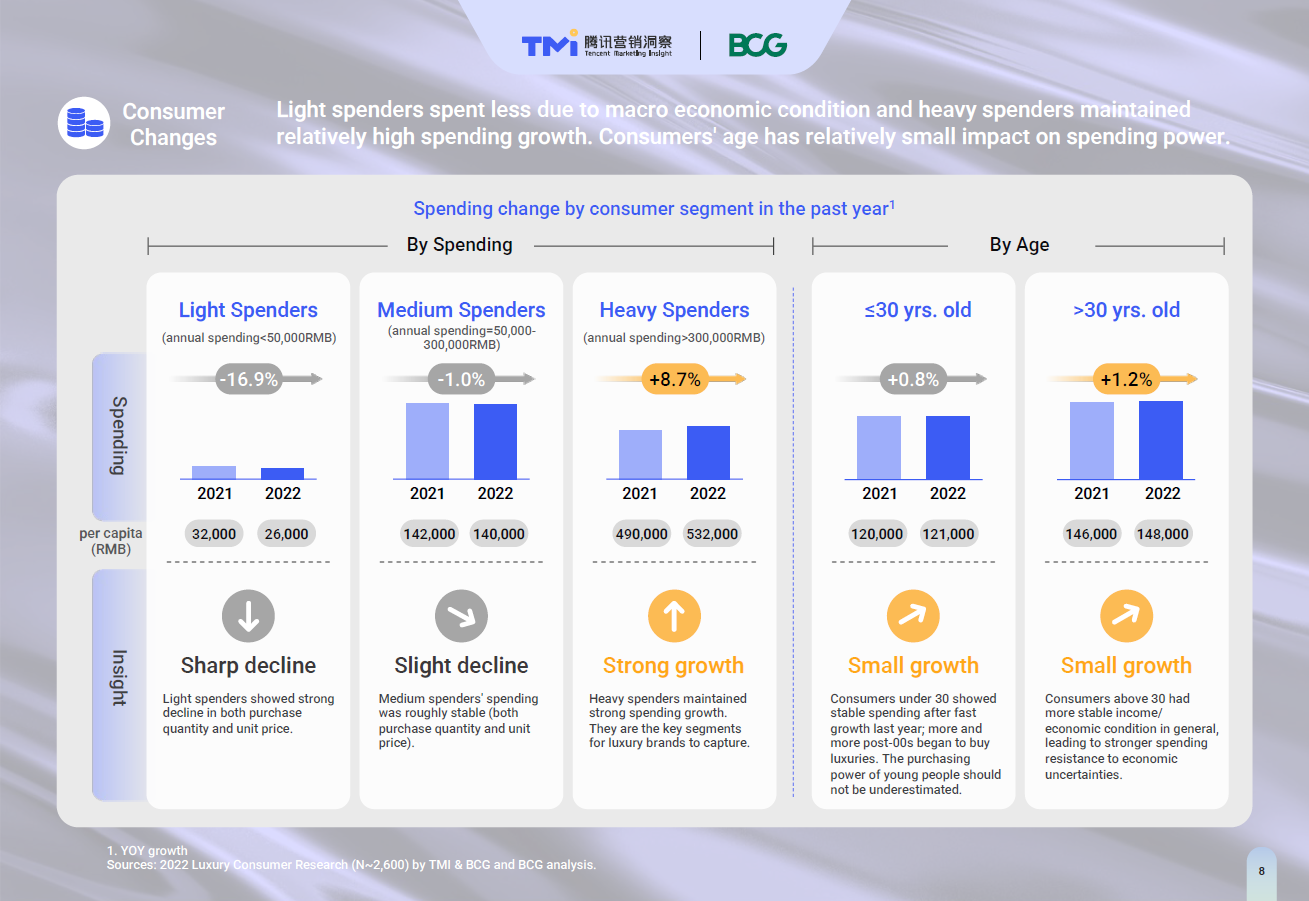

Although the market displayed weak performance over the last year, it is not a lost cause. When spending power in China was examined, mid- and light-spenders (annual luxury spending ≤ 300,000 yuan) were seen to have spent less in terms of volume and unit price in the past year – but the annual spending of heavy spenders (annual luxury spending > 300,000 yuan) grew significantly, reaching 532,000 yuan in 2022, marking an increase of 8.7 per cent.

This consumer segment, which accounts for only 11 per cent total consumers, contributes to nearly 40 per cent of the market. Correspondingly, we observed brands paying even more attention to their VICs in the past year, launching services such as online one-on-one livestream consultations, offline value-added experiences, and even catering meals for VICs during lockdowns.

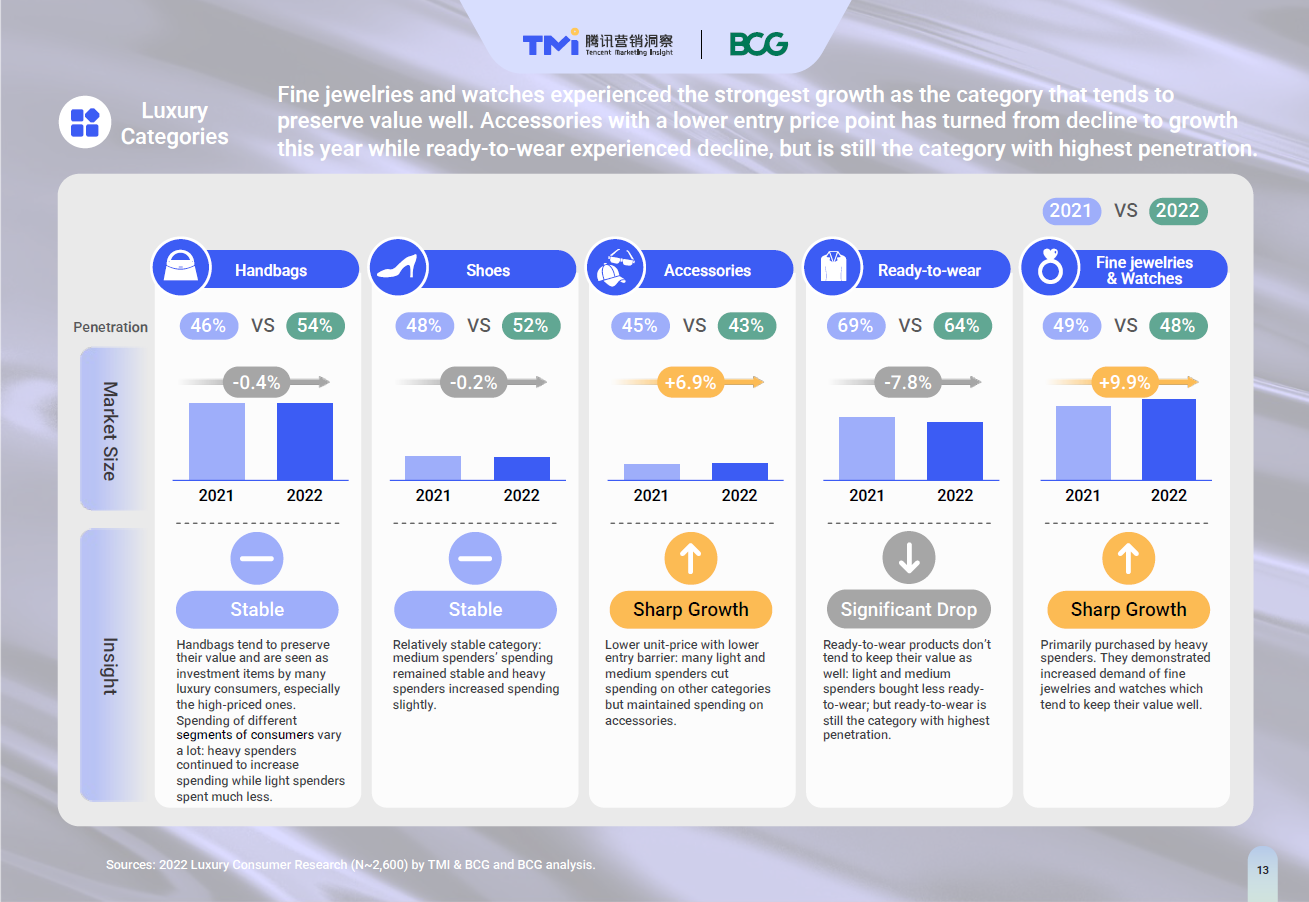

Interestingly, performance across product categories was mixed. The two leading categories, watches and jewellery (up 9.9 per cent) and accessories (up 6.9 per cent), was reflective of two distinct consumer sentiments in today's environment.

The rise of the watches & jewellery category demonstrates demand from high-net-worth individuals who are more interested in high-unit-price items that can hold value during periods of volatility. The rise of the accessories category, however, suggests that newcomers and light spenders remain interested in the luxury world despite challenges in the wider environment.

Additionally, while demand for leather goods and footwear remains stable, sales for ready-to-wear has fallen.

Digital Channels Should Not Be Neglected

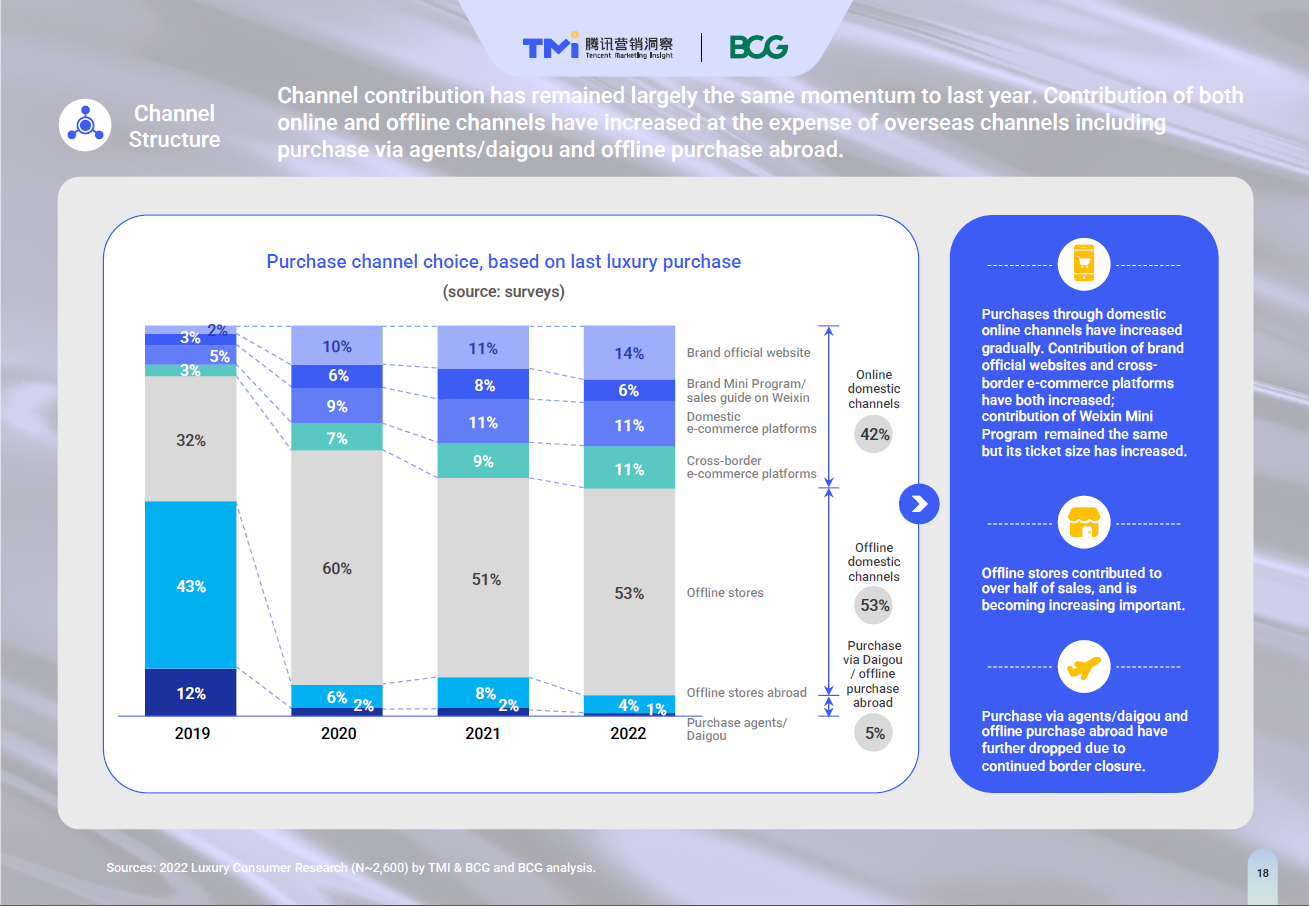

In 2019, the penetration of digital channels in this country was only 13 per cent, but by 2022, the penetration of local online channels – including brand.cn, Mini Programs, and marketplaces – reached 42 per cent. The frequency of online purchases for emerging luxury shoppers is already close to 50 per cent, illustrating the significance of online channels for brands looking to expand their reach.

However, brands should differentiate their strategies across various transactional channels. According to BCG’s research, brand.com and Mini Programs – two DTC channels in China – have the highest per capita spending, at 142,000 yuan and 135,000 yuan, respectively, surpassing even that of offline channels. These channels tend to cater to returning customers who prefer new collections and limited editions, and who have more purchasing power, as well as a greater understanding of the brand and their own demands.

Domestic online marketplaces, on the other hand, have the lowest average spending at 107,000 yuan per year. These days, brands tend to rely on e-commerce platforms like Tmall and JD.com as a critical channel for selling entry-level and classic products, taking advantage of the low threshold for acquiring new customers.

The report also emphasises that online channels are used for more than just transactions. Brand-owned channels have become increasingly important for generating interest and deepening consumer relationships after purchase. Even online market purchases can have a greater impact than social media at the top of the funnel.

Key Segments to Watch

The report identifies three key segments that luxury companies should keep an eye on. Aside from high-spending consumers, post-2000s and male consumers are also promising segments.

Male consumers now make up 43 per cent of the total luxury market, and their proportion of mid- and heavy-spenders is higher than that of female consumers, demonstrating even greater potential in terms of spending power.

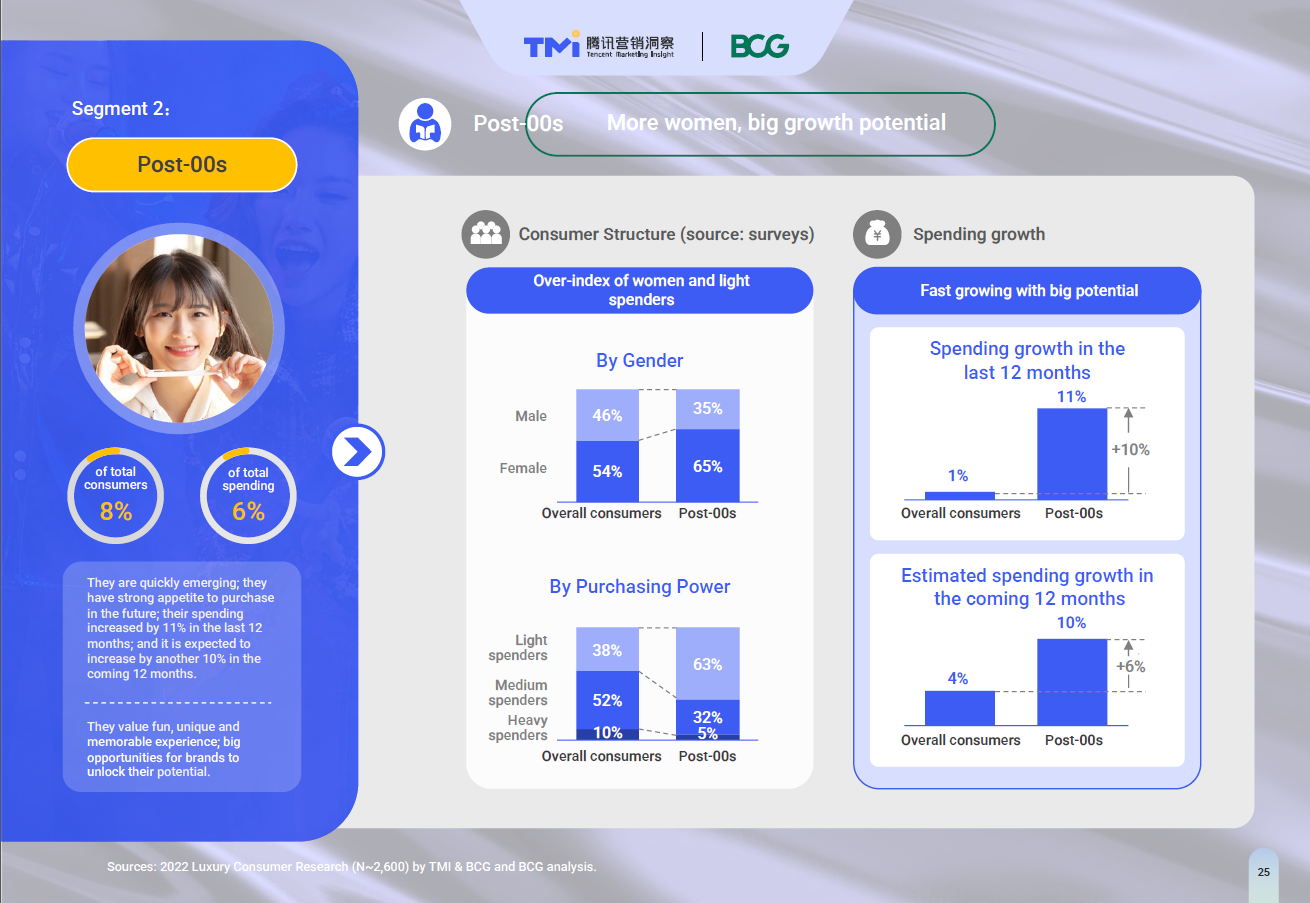

Another key audience segment, the post-00s generation, now accounts for nearly one-fifth of the incremental market share, and the market size of this segment is expected to grow at a rate of 10 per cent in the coming year, exceeding the market average of 4 per cent.

Coupled with the maturation of Millennials and Generation Z in recent years, luxury companies have recognised that these consumers not only represent additional sales figures, but also shape the future of luxury.

Over the last decade, these digital natives have inspired the industry's digital transformation, urging brands to move their communication and transaction activities online. Younger generations are now also pressuring companies to upgrade their digital infrastructures in order to meet their increasingly sophisticated and diverse needs across digital territories. At the same time, their perception of luxury and consumption culture is driving change in the luxury world, pushing leading brands to break down cultural barriers and explore social issues as they navigate today’s world.

Welcome to Data Digest, our breakdown of the latest data releases and reports focused on the luxury industry.